24/7 Emergency Service

24/7 Emergency ServiceHow Do You Estimate Fire Damage to a Commercial Building?

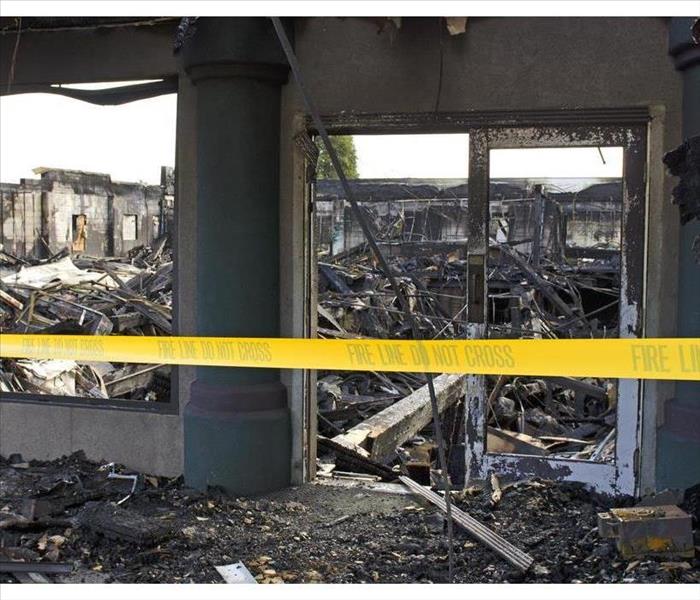

2/4/2021 (Permalink)

Commercial fire damage in Oakford, PA

Commercial fire damage in Oakford, PA

After a commercial fire in Oakford, PA, you’ll need to get an estimate for the repairs to your building. Depending on your insurance company and the policy, this will most likely be developed by the restoration company in conjunction with your insurance adjuster.

However, having some knowledge about what’s involved can help you understand the process and note anything that’s of concern. Some insurance companies can try to reduce the payout, so it’s best if you know your rights.

What Are the Basic Factors Impacting Your Estimate?

Your insurance policy may have limitations, exclusions and riders that will alter your payout. The deductible, or the portion of the damages you’re required to pay, will also vary. Overall, there are three causal factors that impact the cost to repair fire damage:

- How much of your building was damaged.

- The type and purpose of the building.

- The market value of your building.

How Bad Is Smoke Damage?

A major part of the appraisal is based on smoke damage. Smoke is insidious; it gets everywhere, finding tiny gaps and embedding itself into anything remotely porous.

Cleaning up the odor and toxic residue requires very specialized equipment and disinfectants in Oakford, PA. Always choose a local company with plenty of experience in deep cleaning and odor removal. They’ll have high-volume air scrubbers and heavy-duty odor absorbers that strip the oily residue away. Highly absorbent items such as carpet and drywall far removed from the flames still may have to be fully replaced.

Do New Repairs Have to Match Existing Areas?

When you receive the estimate, make sure the adjuster has allowed for repairs to appear uniform. The new portions must have a consistent appearance with new materials and paint matching what already exists. New construction shouldn’t be noticeable to the casual eye.

Some policies will also include lost possessions. Also, you can get a rider to cover your loss of normal business during repairs or other interrupting events. This type of insurance can be expensive, so talk with your agent to determine what’s best for you.